The Nasdaq-100 Technology Sector The index has posted an impressive 414% gains over the past decade, outperforming S&P 500 index gains 185% by huge margin. A key reason why tech stocks have outperformed the S&P 500 during this period is because of their ability to deliver impressive growth as they can capitalize on disruptive trends. This is exactly why it would be a good idea for investors to buy and hold high-tech stocks for the long term.

Super Micro Computer (NASDAQ: SMCI) and Oracle (NYSE: ORCL) are two tech stocks that benefit artificial intelligence (AI)the latest disruption in the world of technology that affects many industries and is expected to contribute significantly to the global economy.

Let’s look at the reasons why buying and holding these tech stocks for the next decade could prove to be a smart move.

1. Super Micro Computer

Super Micro Computer makes server and storage solutions, and the stock is on fire in 2024 with a stunning 208% gain already. However, Super Micro Computer still remains a top tech stock to buy and hold for the next decade for three simple reasons.

First, the company operates in a market that has received a huge boost thanks to artificial intelligence. According to Statista, the AI server market is projected to generate a whopping $430 billion in revenue in 2033 compared to $31 billion last year. This translates to a compound annual growth rate of 30%.

The second reason to buy Supermicro is that it is becoming a key player in this lucrative market. This is evident from the fact that it is growing at a faster rate than the AI server market. The company’s revenue for fiscal 2024 (which ended June 30) is expected to reach $14.9 billion, which would more than double the $7.1 billion in revenue it generated the previous fiscal year.

The fact that Supermicro is outperforming the AI server market is an indication that it is becoming the most popular provider of AI server solutions. As it turns out, Supermicro is too outperforming the established players such as Dell Technologies. Mainly, KeyBanc Analyst Thomas Blakey expects Supermicro’s AI server market share to grow to 23% this year, a level it will likely maintain in the future thanks to its competitive advantages.

If this is indeed the case, Supermicro’s revenue could grow significantly in the long term thanks to the potential size the AI server market is expected to reach. This brings us to the third reason why buying this stock seems like a no-brainer now in light of the potential growth it could deliver.

Super Micro trades at just 4.4 times sales right now, which is lower than the Nasdaq-100 Technology Sector’s 7.4 times sales multiple. Also, the forward earnings multiple of 25 is lower than the index’s reading of nearly 30. With Supermicro’s earnings expected to grow at an annualized rate of 62% over the next five years, buying this AI stock looks like a smart move.

2. Oracle

The spread of artificial intelligence is also lifting Oracle’s boat. This is evident from the company’s recent quarterly reports, which indicate an improvement in demand for its cloud infrastructure offerings.

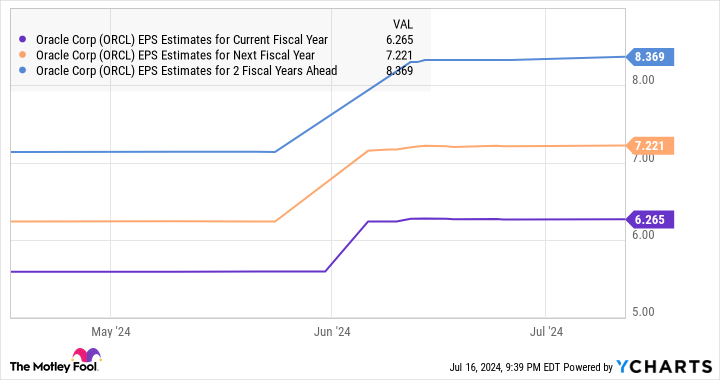

For example, Oracle’s remaining performance obligations (RPOs) in the fourth quarter of fiscal 2024 (ended May 31) rose 44% year over year to $98 billion. That was faster than the 29% year-over-year increase in fiscal third quarter RPO to $80 billion. This faster growth in Oracle’s RPO — which refers to the value of a company’s future contracts that have yet to be fulfilled — points to an improvement in its future revenue line.

Management expects its revenue pipeline to continue to improve due to growing demand for cloud-based AI services. According to a statement from CEO Safra Catz: “During fiscal year 2025, I expect continued strong AI demand to push Oracle’s sales and RPO even higher — and drive double-digit revenue growth this fiscal year. I also expect that each successive quarter should grow faster than the previous quarter — as OCI capacity begins to match demand.”

It’s worth noting that Oracle’s fiscal 2024 revenue rose 6% year over year to $53 billion. So the forecast for double-digit growth in the new financial year suggests that AI is indeed going to drive stronger growth for the company. Another important point to note here is that Oracle signed more than 30 AI sales contracts worth more than $12.5 billion last quarter. That number is very close to the $14.3 billion in revenue the company generated in the fiscal quarter.

As such, AI is already moving the needle in a significant way for Oracle. The good thing is that this trend is here to stay, as the demand for cloud AI services is predicted to take off significantly in the long term. Fortune Business Insights estimates that the cloud AI market could grow from $60 billion last year to nearly $398 billion in 2030, at a compound average growth rate of nearly 31 percent.

As a result, Oracle’s cloud business has a lot of room for future growth, which will positively affect the company’s overall business development. Not surprisingly, analysts are predicting healthy double-digit earnings growth from Oracle over the next three fiscal years after a tepid growth of just 8% last fiscal year to $5.56 per share.

With Oracle shares trading at just 23 times forward earnings right now, a discount to the Nasdaq-100 multiple, now would be a good time to move on. Thanks to the multibillion-dollar opportunity in the cloud AI market, it could deliver more profits over the next decade.

The stock is already up 35% in 2024, and it wouldn’t be a surprise to see it move higher thanks to the stronger growth it’s expected to deliver.

Should you invest $1,000 in a Super Micro Computer right now?

Before you buy shares in Super Micro Computer, consider the following:

The Motley Fool Stock Advisor The analyst team has just identified what they think it is 10 best stocks for investors to buy now… and the Super Micro Computer was not one of them. The 10 stocks that made the cut could produce huge returns in the coming years.

Think about when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you would have $722,626!*

Equity Advisor provides investors with an easy-to-follow plan for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks every month. The Equity Advisor service has more than quadrupled the return of the S&P 500 since 2002*.

*Stock Advisor returns from July 15, 2024

Tough Chauhan has no position in any of the listed shares. The Motley Fool has positions and recommends Oracle. The Motley Fool has one disclosure policy.

2 Tech Stocks You Can Buy and Hold for the Next Decade originally published by The Motley Fool

Leave a Reply